My Sudden Infatuation with Oil

حبي للنفط

8-min read

Everything comes full circle. After attempting to reverse engineer a cracked version of Turmoil (a simulation game in which you drill for oil and expand on your capitalistic tendencies) earlier this year — I now start my investment foray into the hottest liquid commodity.

All information provided in this report is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. One can safely assume the author holds a position in any discussed security. Their economic interest is subject to change without notice.

Two Sides of the Same Lubricated Coin

When it comes to physical oil, there are different grades. The two most popularly traded are:

Brent North Sea Crude (commonly known as Brent crude) and

West Texas Intermediate (WTI).

Brent refers to oil that is produced in the Brent oil fields and other sites in the North Sea.

I use $BNO to track Brent, $USL to track the latter, and $DBO to cover the entire liquid gold commodities market, which has a mixture* of mutual funds, United States Treasury Bills dated for the end of Feb + mid-March ‘21, Invesco’s CLTL, and ~200 basis points of USD Currency. DBO also provides exposure to light sweet crude oil (WTI), which is the most popular oil benchmark in the world. Now one might ask why I’m not adding $USO to my ETF/ ETN basket. Surely with one of the (comparatively) lower expense ratios (0.73% compared to the category average of 0.76) and largest assets ‘under management’ ($3.65BB), and the added advantage of decent liquidity if I wanted to sell at short notice, I’d jump on the proverbial cargo boat. The issue is the relatively higher price and along the same line contango. From the Investopedia page:

Contango is a situation where the futures price of a commodity is higher than the spot price. In all futures market scenarios, the futures prices will usually converge toward the spot prices as the contracts approach expiration. Contango tends to cause losses for investors in commodity ETFs that use futures contracts, but these losses can be avoided by buying ETFs that hold actual commodities.

I choose USL because as its name suggests, they diversify across multiple maturities and rebalance on expiry, potentially eliminating the adverse impacts of contango.

USO suffers from severe contango making it more appropriate for short-term traders.

I guess I’m growing up and turning into a ‘seasoned investor’. Also — why not invest directly in the futures market to bypass this nonsense? Nope. I’ve tried and failed (read: my brief stint in soybeans, culminating in a piqued interest and eventual pivot to insect feed farming). If I’m dipping my toes again in commodities I’ll only stick to exchange-traded funds (or notes). As the Invesco description rightly states:

This product may be a good choice for investors looking to gain exposure to futures contracts on fossil fuels, but do not want the risks associated with a futures-contracts.

I digress. Year-to-date, they’re all doing horribly. Across the board, they’ve lost ~30% of their value, with outlier USO taking a huge hit of 68.61%. But since the time I exposed myself to the oil & gas sector, which was about twelve weeks ago, month-on-month they’ve consistently gained 3-4%.

YTD Performance for select O&G ETFS, ranked by assets (in ascending order) --

USO: -68.61%

DBO: -22.96%

UNG: -42.94%

BNO: -39.86%

USL: -27.05%

UGA: -30.01%

OILK: -61.95%

DBE: -27.28%

OIL: -27.52%

UNL: -5.13%

GAZ: -39.29%

RJN: -46.51%

JJE: -42.95%

Data from etfdb, dated Dec 16, 2020* I really wanted to use emulsion here instead.

Some Barely Passable Technical Analysis

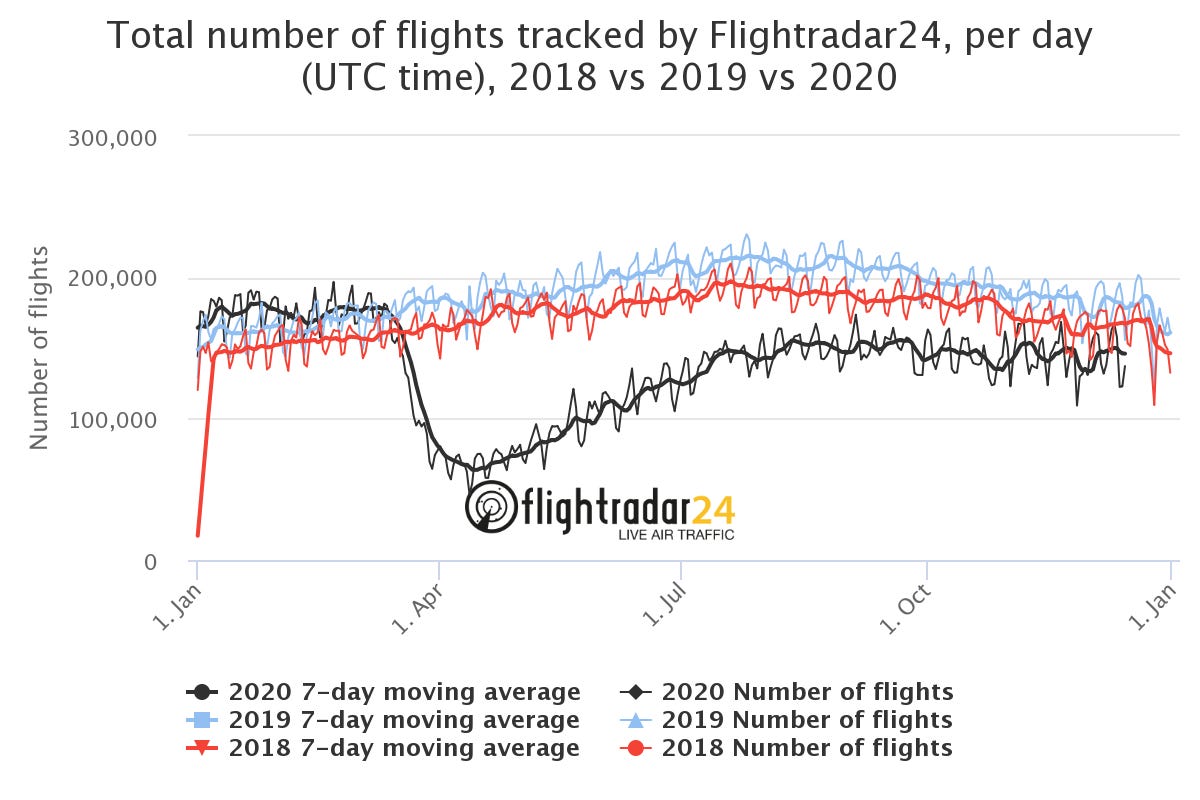

Now the burning question — why am I switching gears in the final month of the final quarter of 2020 from my usual tech and biopharma plays to not only an entirely different sector but a totally unrelated industry? I believe oil is poised to make a huge comeback next year. This year, and the pandemic, has been particularly brutal on our beloved time-tested corporations and combined with a huge demand and a dramatic increase in Airbnb rentals and pickup in flights (especially on Thanksgiving), we’re looking at a complete overhaul for shale. Now, some cool graphs!

and

Now one might look at the actual dataset from TSA checkpoint travel numbers and point the number-of-passengers discrepancy, but why should I care? Sure, total traveler throughput has fallen 33% compared to last year, but flights are still being chartered. Also, the initial investment is literal pennies on the dollar after COVID-19 ravaged the market. Warren Buffet seems to agree with my acuity:

Buffett has a reputation for spending his money fairly parsimoniously. Meaning he buys good companies when they are cheap, and famously, rarely sells them. I think there are two things that he likes about the pipeline business. One, it's a tolling business with long-term take or pay-type contracts and without nominally much exposure to commodity prices, although as we have seen those chickens will eventually come home to roost. And, as WB has told us previously, he likes businesses where he can just collect fees.

Read: Why Warren Buffet Is Betting Big On Oil & Gas Pipeline Companies

Disclaimer: I wouldn’t pay too much heed to information from a website named oilprice.com but they do have some neat insights.

We’re slowly converging on the equilibrium point, akin to contango!

Let’s correlate random data together and compare our ETF/ ETNs 2-year charts to another prominent oil player of the S&P 500 (which recently closed around mid-40s — laughable after holding the #1 spot in 2008): Exxon, ticketed as XOM.

Correlation = Causation?

One would expect similarities between a company whose primary industry focus is Oil, but comments by current CEO Darren Woods suggest otherwise:

‘I believe the assumption that affordable energy and a cleaner environment are a zero-sum game is mistaken. It underestimates the power of technology. The zero-sum view is a static one, and the world of energy is anything but static. But technology changes the equation. It makes a dream – growing the economy while reducing emissions – a reality.’

Read: ExxonMobil and Global Clean Energy Holdings sign agreement for renewable diesel — Aug ‘20

Interesting take from a Rockefeller company, especially when in 2015 they prefaced a shareholder meeting with the then CEO making fun out of clean energy by commenting ‘We Choose Not to Lose Money on Purpose’. He then went on to get nominated as Secretary of State by then-President-elect Donald Trump on December 14, 2016, almost retiring four months early and potentially giving up a $180MM retirement package. He did redeem himself later:

following Trump’s strangely political and inappropriate speech at the annual Boy Scout Jamboree, Tillerson, according to NBC, was so offended that he was going to resign, until Vice-President Pence, Defense Secretary James Mattis, and the incoming chief of staff, John Kelly, persuaded him to stay. That same month, Mattis reportedly attended a meeting of national-security officials at which Tillerson referred to Trump as a ‘fucking moron.’

Read: Rex Tillerson at the Breaking Point — Oct ‘17

And I don’t want only want to shame Exxon alone. BP, Shell, Eni, Chevron all have reneged on their idealistic green-thumbed promises:

Despite the growth in renewables, big oil only spent 1% of its combined budget on green energy schemes in 2018.

A 2019 report by Matthias J Pickl — an economics professor at King Fahd University of Petroleum and Minerals in Saudi Arabia — discussed whether oil companies are transforming themselves into energy firms.

Furthermore, growing concerns about climate change following the Paris Agreement may provide an additional drive for such strategy to hedge against hardening investor sentiment towards carbon emissions.

Playing Devil’s Advocate

Why is it so difficult to predict oil trends? Well, we’re living in tumultuous times.

Short-sellers (like me) have lost more this year on Tesla than ever before.

According to analysis by S3 Partners, short investors in Tesla— those who placed bets in the market that its shares would lose value — have lost $35 billion on those positions so far this year. To put that loss into context, the US airline industry posted combined net losses of $24.2 billion, excluding special items, through the first nine months of 2020, the worst losses the industry has ever reported.

The automobile company is also poised to join the S&P 500 with a 1.5% weighting (compared to Apple’s 5.8%) on Monday, December 21, 2020. And I would prefer not to comment on Musk’s meteoric rise from multi-billionaire to current Twitter meme-lord. In a span of 9 hours on December 14th, he shared these golden nuggets:

Will this one trade put me in the black for the next year? I’m not sure. These publicly listed companies have to deal with new regulations, comply with ESG principles, and face the highest possible level of government scrutiny before they stand a chance of turning a profit in ‘21. Oil supply is currently outcompeting demand, and we might never go back to the way it was before. And if you look at the 5-year-window of any O&G corp you see red lines and losses. It might already be too late — the gold rush is finally over. How am I hedging my bets? I’m being less risky, by investing in ETFs of commodities instead of the futures market, but also riskier, because of the incontrovertible proof that oil is a dangerous business and I’m probably way over my head. But combined with stop losses and my unnervingly high-risk profile (thanks to crypto), I do believe oil will make a good enough comeback to lock in profits. I would like to close on two questions:

Will the R² of these big conglomerates stocks and oil ETFs continue along with these trends or show some meaningful divergence in the near future?

And when?

I don’t believe they’re going to be changing teams anytime soon, but nevertheless, I’ve included more resources below for you to accurately judge and ponder for yourself:

Exxon Quietly Researching Hundreds of Green Projects — Nov’ 17

ExxonMobil’s Failure to Go Green Could Worsen Its Financial Future — Nov’ 20

I’ll leave this as an exercise to the reader on where the road less taken (and frankly hopefully less polluted) might take us. Also, please let me know so I can exit some positions.

Further Reading

Shell, Eni Settle Dispute With Kazakhstan in $1.3 Billion Deal — Dec ‘20

The deal unlocks plans to boost output from the Karachaganak [oil] field.